Receiving a sales tax audit notice from the Florida Department of Revenue can feel overwhelming. But the end of an audit does not necessarily mean the end of the road. Florida taxpayers have powerful legal tools to challenge assessments they believe are inaccurate and understanding how to use them can make the difference between paying a large bill and walking away with a fraction of the original assessment, or nothing at all.

The Audit Is Over. Now What?

After an auditor completes a Florida sales tax audit, the Department issues a Notice of Intent to Make Audit Changes. This document summarizes the initial assessment, including any tax, interest, and penalties. At this stage, many taxpayers assume the number is final. It is not.

Taxpayers have the right to meet with the auditor's supervisor, provide additional documentation, and negotiate revisions before the assessment is formally issued. This informal phase is often underutilized but can be extremely valuable, particularly when the audit relied on estimates, sampling errors, or misclassified transactions.

The Informal Protest: Your First Line of Defense

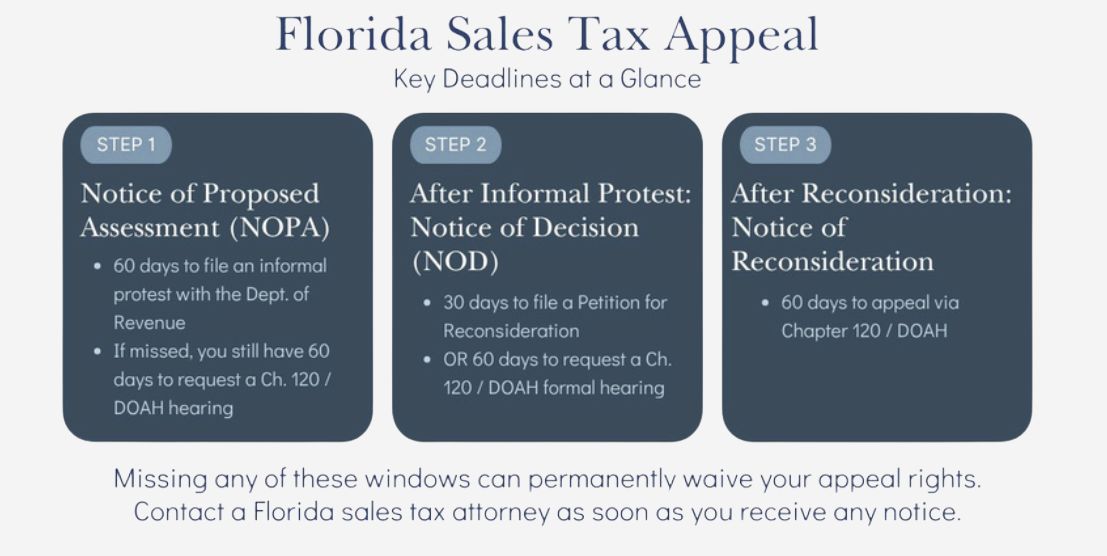

Once a Notice of Proposed Assessment (NOPA) is issued, the clock starts. Taxpayers have 60 days to file a written protest with the Department of Revenue.

This protest must:

- Clearly identify the contested assessment

- State the specific grounds for the protest

- Include any supporting facts, evidence, and legal authority

Filing a complete, well-supported protest is critical. A vague or incomplete protest may waive important rights and limit your options at later stages. If the Department issues a Notice of Decision (NOD) denying the protest, the taxpayer then has 30 days to file a Petition for Reconsideration or 60 days to escalate directly to a Chapter 120 formal hearing at DOAH. If the taxpayer pursues reconsideration and the Department issues a Notice of Reconsideration (NOR), there is an additional 60-day window to appeal via Chapter 120. Importantly, a taxpayer who never files an informal protest at all still has 60 days from the NOPA to request a Chapter 120 hearing directly.

Chapter 120: Florida's Administrative Procedure Act

Chapter 120 of the Florida Statutes governs how state agencies, including the Department of Revenue, must conduct contested case proceedings. When a taxpayer requests a formal hearing, the case is typically transferred to the Division of Administrative Hearings (DOAH), an independent body that assigns an Administrative Law Judge (ALJ) to hear the dispute.

This process offers taxpayers several significant advantages:

- An impartial judge, not a DOR employee, decides the legal and factual issues

- Both sides can conduct discovery, take depositions, and subpoena records

- The formal rules of evidence apply, giving experienced tax counsel important procedural tools

- The ALJ issues a Recommended Order, which the Department must then formally adopt, reject, or modify, providing a clear record for further appeal

What Happens After DOAH?

Once the ALJ issues a Recommended Order, the Department of Revenue enters a Final Order. If the Final Order is unfavorable, the taxpayer may appeal to the First District Court of Appeal. Alternatively, a taxpayer who has paid the assessment may file a refund claim in circuit court, bypassing the administrative process entirely.

Choosing the right path, administrative protest vs. refund litigation, depends on the nature of the dispute, the amount at issue, and the taxpayer’s risk tolerance. There is no one-size-fits-all answer, and selecting the wrong forum can result in procedural hurdles that cost time and money.

Common Audit Issues Worth Contesting

Not every assessment is worth challenging, but many audits contain errors that a skilled tax attorney can identify and successfully dispute. Some of the most common include:

- Improper sampling methodology that inflates the assessed tax

- Misclassification of exempt sales (e.g., resale, manufacturing, agriculture)

- Failure to credit documented tax paid to vendors

- Incorrect application of local surtax rates

- Transactions subject to a different tax (such as use tax already remitted)

- Assessments based on records the auditor misread or misunderstood

Even when the original assessment has some merit, experienced representation in the protest phase often results in a meaningfully reduced final number.

The Bottom Line

A Florida sales tax assessment is not a bill you must simply pay. The protest process and Chapter 120 procedure exist specifically to give taxpayers a fair opportunity to challenge assessments they believe are wrong. However, not all Chapter 120 petitions must go before an administrative law judge. Many Chapter 120 petitions get settled by Department of Revenue attorneys before going to court, which can be a much more cost-effective way to get a fair result. But these rights must be exercised correctly, and on time.

If your business has received an audit notice or a proposed assessment, the most important step you can take is to contact an experienced Florida sales tax attorney before the deadline passes.