The U.S. Mint has stopped producing pennies, and Florida just passed a law telling every cash-accepting business how to handle the sales tax math that follows. If you run a retail store, restaurant, convenience store, salon, or any other business that still takes cash, this is not a "someday" problem. Pennies are already getting scarce in cash drawers across the state, and the Florida Legislature did not leave it to chance how dealers should round transactions or, more importantly, how that rounding interacts with the sales tax you are legally required to collect and remit.

This article walks through what changed, what stayed exactly the same, and what you and your accountant need to do at the point of sale starting now. The article is written by James H Sutton, Jr, CPA, Esq, an attorney that focuses almost exclusively on Florida sales tax controversy.

WHY THIS HAPPENED

The federal government has stopped manufacturing new one-cent coins because, simply put, it costs more than a penny to make one. The Treasury Department has made clear that pennies remain legal tender and that the roughly 114 billion pennies already in circulation will keep moving through the economy as people spend them. But "still legal tender" and "still available in your cash register" are two very different things. As pennies thin out, cashiers increasingly cannot make exact change on cash transactions, particularly when the total ends in an odd one or two cents.

The Florida Department of Revenue saw this coming before the Legislature did. In December 2025, DOR issued Tax Information Publication 25A01-18, giving dealers interim guidance on how to round cash totals without shortchanging the state. The Legislature then took that guidance and wrote it into the Florida Statutes through CS/SB 1074 (companion bill CS/CS/HB 951), sponsored by Senator Gaetz in the Senate and Representatives McFarland and Overdorf in the House. The bill was signed into law by Governor DeSantis in May 2026, took effect immediately upon signing, and is now Chapter 2026-68, Laws of Florida. It amends section 212.12, Florida Statutes (the dealer's-credit-and-rounding statute), section 501.212, Florida Statutes (the Florida Deceptive and Unfair Trade Practices Act), and section 538.235, Florida Statutes (governing payments to secondary metals recyclers).

THE NEW RULE, IN PLAIN ENGLISH

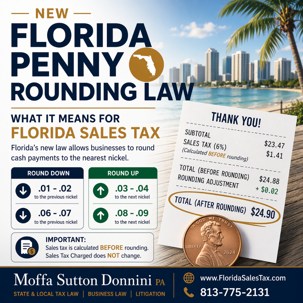

The statute now permits a dealer to round the total amount due on an in-person cash transaction to the nearest nickel when the dealer cannot make exact change because pennies are not available. The rounding is applied to the final amount due, after sales tax (and any discretionary surtax) has already been added to the sales price. The methodology is simple:

If the final digit of the total is 1 or 2 cents, round down to 0 cents. If the final digit is 3, 4, 6, or 7 cents, round to 5 cents. If the final digit is 8 or 9 cents, round up to 10 cents. Totals already ending in 0 or 5 cents are not rounded at all.

A quick example: a taxable item priced at $9.84, taxed at a combined 7% rate, produces a pre-rounding total of $10.53. Under the new methodology, that 3-cent ending rounds up to $10.55. A total of $10.51 or $10.52 would round down to $10.50.

The law defines "cash" the way federal banking law does: United States coins and currency, including Federal Reserve notes. That definition matters because it tells you exactly where this rule does and does not apply.

WHAT DOES NOT CHANGE

This is the part business owners most need to internalize, because it is also the part most likely to get a dealer in trouble if misunderstood.

Sales tax is still calculated on the exact, unrounded sales price. Nothing in this law changes the tax base, the tax rate, or the amount of tax legally due to the state. Rounding only touches the cash actually handed across the counter at the very end of the transaction. Your point-of-sale system should be calculating sales tax the same way it always has; the rounding step happens after that calculation, not instead of it.

Electronic and non-cash payments are entirely unaffected. Credit cards, debit cards, gift cards, checks, money orders, and ACH transfers settle for the exact amount due, down to the penny, regardless of whether physical pennies exist. If a customer pays the cash portion of a split transaction in cash and the rest electronically, only the cash portion gets rounded.

You still owe the full, exact tax. Whatever you collect at the register because of rounding, up or down, you remit the actual tax due based on the unrounded sales price. If rounding works in the customer's favor on a given transaction, that is not a basis to remit less tax than the law requires. If it works in the dealer's favor, that is not additional taxable revenue either; it is simply a function of correct change-making.

Rounding correctly is not a deceptive trade practice. The new law adds a specific exemption to the Florida Deceptive and Unfair Trade Practices Act stating that rounding a cash sale to the nearest nickel, done consistently with the statute, is not a violation. That protects dealers who follow the methodology from a category of consumer-protection claims that might otherwise have been threatened by an enterprising plaintiff's lawyer once this practice became widespread.

There is also a parallel provision addressing cash payments made to secondary metals recyclers, who operate under different statutory payment requirements than ordinary retail dealers, so businesses in that industry should look at section 538.235, Florida Statutes, directly rather than assuming the general retail rule covers them identically.

PRACTICAL STEPS FOR BUSINESS OWNERS AND THEIR ACCOUNTANTS

Talk to your point-of-sale vendor now. Most modern POS and payment-processing systems will need a configuration update, not a full system overhaul, to apply nickel rounding automatically to cash transactions while leaving electronic transactions untouched. Confirm your system separates the tax calculation step from the cash-rounding step; if it does not, you risk under-collecting or over-collecting tax rather than simply rounding the change.

Post a sign. The DOR's TIP and the legislative history both emphasize disclosure. A short, clearly visible sign at the register or counter explaining that cash transactions may be rounded to the nearest nickel when pennies are unavailable protects you from customer confusion and gives you a documented, consistent practice if anyone ever questions a transaction.

Pick one method and apply it consistently. The statute's rounding table removes the guesswork, but only if you actually program it in and use it the same way every time. Ad hoc, cashier-by-cashier rounding decisions are exactly the kind of inconsistency that invites scrutiny.

Keep your records straight. Your sales tax return should reflect tax calculated on actual sales prices, not on rounded cash totals. If your bookkeeping system or your accountant is reconciling daily cash drawer totals against reported sales, build in an understanding that small, immaterial rounding differences between cash collected and tax remitted are expected and explainable under this law, not a sign that something is wrong.

Remember this is a cash-only issue. If your business is primarily card-based, online, or otherwise rarely handles physical cash, this law has limited day-to-day impact on you, but it is still worth confirming your few cash transactions are handled correctly.

QUESTIONS BUSINESS OWNERS ARE ASKING

Does Florida's new penny rounding law change how much sales tax I owe? No. Sales tax is still calculated and owed based on the exact, unrounded sales price. Rounding only affects the cash amount physically exchanged at the register.

Can I round credit card and debit card transactions to the nearest nickel? No. The rounding methodology under the new law applies only to in-person cash transactions, as defined by federal banking law. Electronic payments settle for the exact amount due.

What rounding method does Florida require for cash sales tax transactions? Totals ending in 1 or 2 cents round down to 0; totals ending in 3, 4, 6, or 7 cents round to 5; totals ending in 8 or 9 cents round up to 10. Totals already ending in 0 or 5 cents are not rounded.

Is rounding a cash sale to the nearest nickel a deceptive trade practice in Florida? No. The new law specifically exempts rounding done in compliance with the statute from the Florida Deceptive and Unfair Trade Practices Act.

What is Florida TIP 25A01-18? It is the Florida Department of Revenue's December 2025 guidance addressing cash rounding due to penny scarcity, issued before the Legislature codified similar rules into statute through Chapter 2026-68, Laws of Florida.

THE BOTTOM LINE

This law solves a real, immediate operational problem without changing a single dollar of sales tax liability. The risk for Florida businesses is not the rounding itself; it is implementing rounding sloppily, mixing it into the tax calculation, applying it to electronic payments, or doing it inconsistently without disclosure. Get your POS configuration right, post the signage, and keep your accountant looped in on how your system is handling the cash drawer versus the tax return, and this is a non-event. Get it wrong, and what should have been a one-time system update becomes an audit conversation about under-collected tax.

About the Author: James H. Sutton, Jr., CPA, Esq. is a CPA and a State and Local Tax (SALT) attorney as well as shareholder at the Law Offices of Moffa, Sutton & Donnini, P.A. Mr Sutton has an almost exclusive practice area in Florida sales and use tax controversy, with offices in Fort Lauderdale, Tampa, and Tallahassee. James can be reached at 888-444-9568, JamesSutton@FloridaSalesTax.com. You can read more about James Sutton in his biography HERE. Take advantage of his FREE INTITIAL CONSULTATION.

About the Author: James H. Sutton, Jr., CPA, Esq. is a CPA and a State and Local Tax (SALT) attorney as well as shareholder at the Law Offices of Moffa, Sutton & Donnini, P.A. Mr Sutton has an almost exclusive practice area in Florida sales and use tax controversy, with offices in Fort Lauderdale, Tampa, and Tallahassee. James can be reached at 888-444-9568, JamesSutton@FloridaSalesTax.com. You can read more about James Sutton in his biography HERE. Take advantage of his FREE INTITIAL CONSULTATION.

ADDITIONAL RESOURCES

DO I HAVE TO CHARGE FLORIDA SALES TAX ON A WHOLESALE SALE?, published June 7, 2026, by James H. Sutton, Jr., CPA, Esq.

CAN I TRUST AI FOR FLORIDA SALES TAX ADVICE?, published June 6, 2026, by James H. Sutton, Jr., CPA, Esq.

FLORIDA SALES TAX – INADVERTENT REGISTRATION: WHAT IT IS AND HOW IT CAN SAVE YOUR BUSINESS, published June 5, 2026, by James Sutton, CPA, Esq.

FLORIDA SALES TAX VOLUNTARY DISCLOSURE: THE BEST WAY TO CLEAN UP A FLORIDA SALES TAX PROBLEM, published May 26, 2026, by James H. Sutton, Jr., CPA, Esq.

DO I NEED A LAWYER FOR A SALES TAX AUDIT?, published June 9, 2026, by James H. Sutton, Jr, CPA, Esq.

FLORIDA SALES TAX FOR E-COMMERCE SELLERS, published June 12, 2026, by James H. Sutton, Jr., CPA, Esq.

FLORIDA SALES TAX ON LABOR, published May 23, 2026, by James H. Sutton, Jr, CPA, Esq.

© Copyright 2026. James H Sutton, Jr. All rights reserved.